Trauma cover, sometimes known as critical illness or living cover is all about supporting your recovery from a serious illness – helping you afford the treatment of your choice and allowing you to make necessary changes to your lifestyle.

When you’re looking at trauma cover, there are 3 key things you need to understand so you know what you’re covered for, and what that means at claim time:

What you can claim for – Trauma definitions

How your cover is structured – Stand-alone or linked

Making multiple claims – Trauma reinstatement

1. Trauma definitions

Every trauma cover policy comes with a list of definitions that dictates:

what medical conditions are covered by your policy

how severe those conditions need to be for a claim to be paid

what percentage of the sum insured will be paid in the event you suffer one of the covered conditions.

Generally speaking, trauma cover is designed to cover you for severe conditions that are likely to require expensive medical treatment, a significant recovery period and/or force you to make major lifestyle changes. It is not designed to cover you for minor conditions that require simple or non-invasive treatments.

For example, you may be diagnosed with a skin cancer that hasn’t spread and is treatable in one procedure. Or you may be diagnosed with an aggressive skin cancer that requires chemotherapy or radiotherapy for months. They’re both technically ‘skin cancer’, but they’re very different in terms of their impact on your life.

You can find the trauma definitions that apply to your policy in the Product Disclosure Statement (PDS), with many of these definitions now standard across the life insurance industry. It is worth reviewing and understanding the differences between policies to ensure you get the best cover for you and your loved ones.

2. Linked covers

Trauma cover may be purchased as a stand-alone policy or as a ‘linked policy’ connected to life cover or TPD cover.

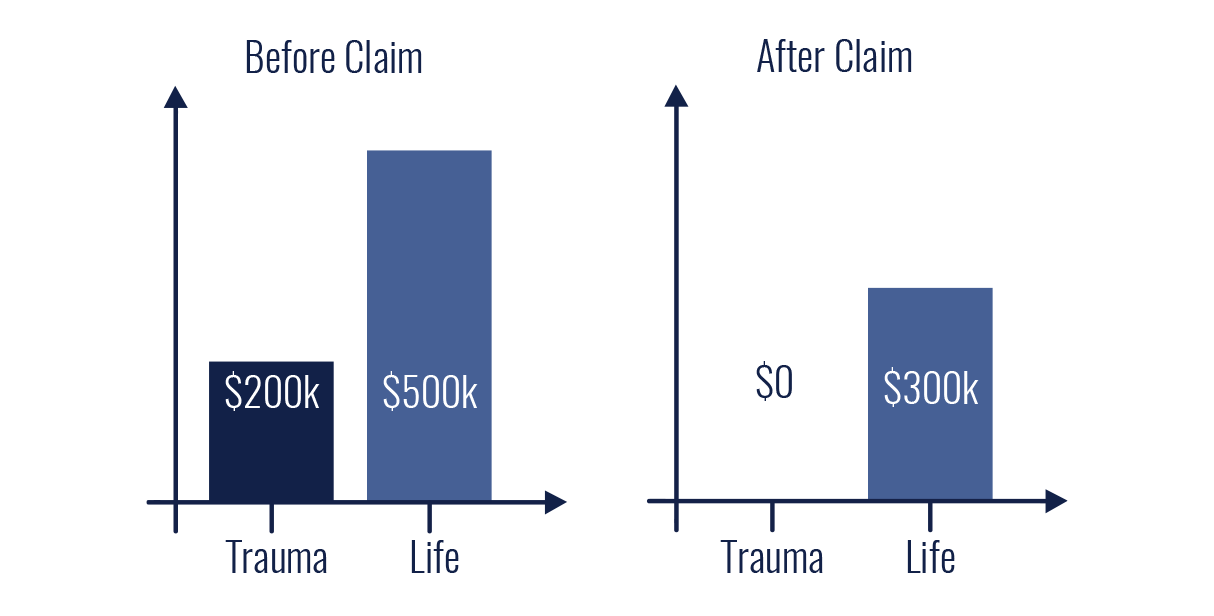

Generally linking policies reduces premiums, but there are implications at claim time. Say you have a $200,000 trauma cover policy linked to a $500,000 life cover policy. If you make a successful claim on your trauma cover, your life cover benefit will reduce by the $200,000 paid out (i.e. to $300,000).

Depending on your situation you may be eligible to buy back this extra life cover at some point, but it’s important to note that your life cover is significantly reduced in the meantime.

3. Trauma reinstatement

A little-known benefit of trauma cover is that you may be able to make multiple claims in your lifetime.

That’s because some trauma cover policies offer a trauma cover reinstatement option after a successful claim. A reinstatement option allows you to recommence your policy, typically 12 months or more after a claim has been paid. Typically a reinstated policy won’t cover you for the same medical condition you already claimed on, or a related condition, but it can still cover you for a wide range of other serious illnesses.

Learn more about Trauma insurance and it’s exclusions in the Product Disclosure Statement, otherwise speak to your financial adviser.

Did you know?

There’s a common exclusion on trauma cover policies that means you generally won’t be covered for some medical conditions if they’re first diagnosed within 90 days of receiving your application. Also you are likely to not be covered for any conditions that directly or indirectly arise from an intentional act or omission. You can find details of any exclusions in your Product Disclosure Statement (PDS).